In this article, we will be discussing the entire process of making a journal entry in QuickBooks Online. You need to check out the following steps in order to create journal entry.

Use the Journal Entry in QuickBooks Online when you have to:

Send Money between income & expense accounts

Transfer money from an asset, liability, or an equity account to the income or the expense account.

In this blog, we will concentrate on How to Create Journal Entry and other essential points related to it.

Rules to Make Journal Entry in QuickBooks Online

Mostly Journal Entries for QuickBooks are done for Income Tax provisions, Depreciation Entries, and Loan interest Adjustments.

To make a journal entry in QuickBooks online you have to include one account receivable or accounts payable.

To know the complete steps read the blog.

Often the QuickBooks users enter the accounting transactions incorrectly into an accounting, and when this happens, the users are required to form changes to the first transaction even after been recorded, and this will be easily wiped-out QuickBooks accounting software, by simply creating a Journal entry.

QB users can make journal entries in QuickBooks Online during a straightforward manner.

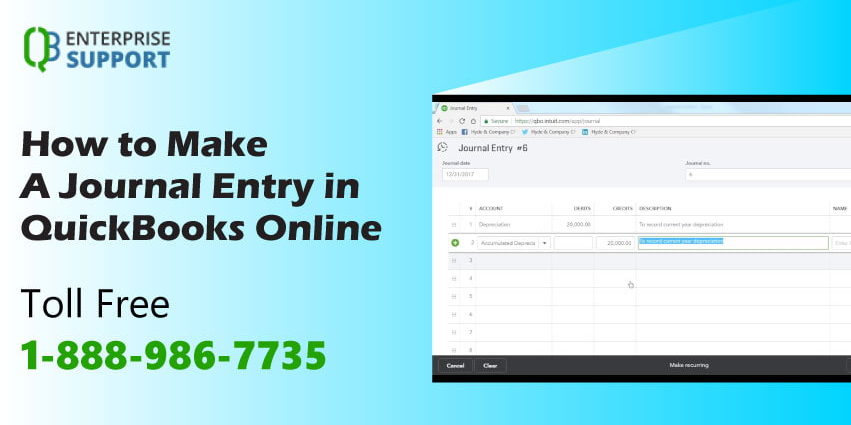

Let’s look how to create a Journal Entry in QuickBooks Online.