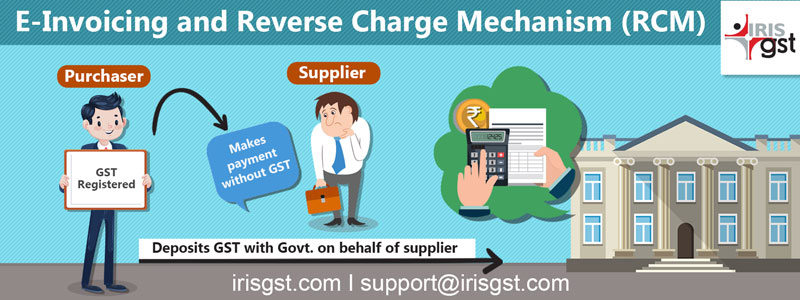

E-invoicing starts in a month and the onus of creating invoices and getting them registered on the Invoice Registration Portal (IRP) lies on the Supplier. This, in a usual scenario can work fine. However, for a business, there are multiple transactions that need to be reported under Reverse Charge Mechanism (RCM). The companies are in a state of confusion on RCM transactions when e-invoice goes live as in the case of RCM, Purchaser issues self-invoice which is reported in GST returns and under E-Invoicing, Purchasers under no situation can generate Invoice Reference Number (IRN).

Let us understand the rules of e-invoicing in relation to RCM

E-invoicing has finally seen the light of the day.

While the Government has provided relaxation to e-invoice mandate subject to certain conditions, e-invoicing is now officially here and the taxpayers have started generating Invoice Reference Number IRN compliant invoices.E-invoicing as much as it impacts the suppliers, it has a ripple effect on the purchase cycle too.

And the consequences of non-compliance by supplier can cost recipient their ITC.

And who wouldn’t want to safeguard themselves against this risk and put checks and processes in place.Know more about e-invoicing and ITC claim.