Pre-insulated pipes are employed in residential, commercial, and industrial buildings to curtail energy losses, maintain temperature, and transport fluids from heating and cooling facilities to these buildings. Thus, the surging construction of residential, industrial, and commercial facilities, owing to the rapid urbanization, will generate a huge requirement for pre-insulated pipes in the coming years. Construction groups, governments, and building owners are adopting pre-insulated pipes to lower the energy footprint during the occupancy of buildings as they are pivotal to energy systems and help in curtailing the energy consumption level.

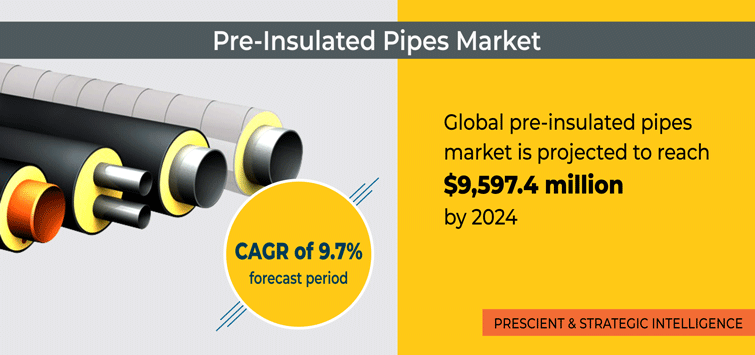

Additionally, the increasing adoption of district heating and cooling (DHC) systems will also drive the pre-insulated pipes market at a CAGR of 9.7% during the forecast period (2019–2024). The market revenue stood at $5,568.5 million in 2018 and it is expected to reach $9,597.9 million by 2024. The commercial and residential sectors of Denmark, Germany, France, Iceland, Russia, China, Japan, and the U.S. are adopting DHC systems in abundance, due to the mounting focus of governments, local energy providers, and community owners on lowering energy consumption monetizing the energy generated from multiple sources, and curtailing energy costs, respectively.

Pre-insulated pipes used in residential, commercial, and industrial facilities are made of metals and polymers. Pipes made of polymers and metals are manufactured by ZECO Aircon Ltd., SA Insulation Pty. Ltd., PEM Korea Co. Ltd., Uponor Infra Fintherm a.s., Rigitech Rigid Foam Products, Thermal Pipe Systems Inc., Polymerteplo Group, and Perma-Pipe International Holdings Inc. Pre-insulated pipes offered by these companies consist of three layers— outer jacket, carrier pipe, and insulation layer. These three-layered pipes are used to transport liquid and gas in the industrial, residential, and commercial sectors.

According to P&S Intelligence, North America was the largest user of pre-insulated pipes in the recent past. This was because of the rising installation of DHC systems across the downtown districts of Canada and the U.S. and the flourishing construction and chemical processing industries in the region. The growing adoption of DHC systems in Canada and the U.S. can be credited to the financial incentives, such as tax breaks, subsidies, grants, and low-interest loans, being offered by the governments of these countries for installing such systems.

Whereas, the European pre-insulated pipes market is expected to exhibit the fastest growth during the forecast period. This will be due to the soaring number of nearly zero-energy buildings (NZEBs), rising adoption of building standards and codes, and surging focus on renovation and retrofitting of old buildings in the region. Besides, the mounting focus of numerous European countries on circular economy will also supplement the market growth in the foreseeable future.

Thus, the flourishing construction industry and escalating installation of DHC systems will augment the adoption of pre-insulated pipes in the forthcoming years.