Payment facilitators are a central pillar of successful businesses, and in this guide, we’ll cover everything there is to know about the topic.

What is a payment facilitator?

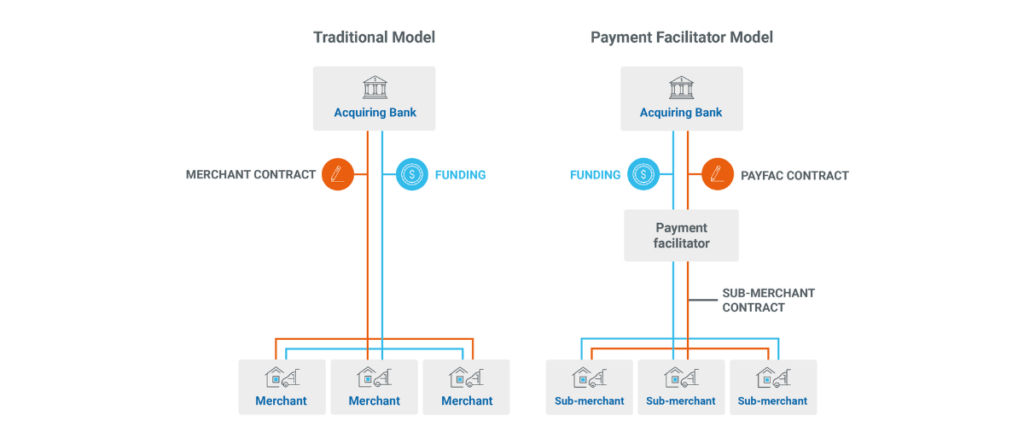

A payment facilitator, also called a PayFac, is an entity that helps companies accept electronic payments from customers via multiple channels by quickly onboarding them as submerchants. Thus, the company can use the PayFac’s infrastructure to easily collect payments from its customers while the PayFac manages all administrative and technical aspects of the infrastructure.

How does the payment facilitator model work?

The payment facilitator model simplifies the way companies collect payments from their customers. It also helps onboard new customers easily and monetizes payments as an additional revenue stream.

Here are the key players in the chain, along with the role they play in the facilitation model.

1. PayFacs

PayFacs manage the back-end processes associated with online payments. For instance, they provide merchants with payment infrastructure, maintain payment channels, and secure all associated technology.

Most PayFacs provide payment analytics that helps merchants analyze cash flow trends in their accounts, payment channels, and customers.

Thanks to additional services like fraud checks and seamless integration with third-party apps, PayFacs are a one-stop-shop for everything connected to payment acceptance.

2. Submerchants

A submerchant is a company that uses a PayFac to offer customers online payment channels. For instance, a SaaS vendor that offers its clients the ability to Collect credit card payments is a PayFac and its clients are submerchants.

PayFacs verify a company’s documents before onboarding. These checks are necessary to fulfill KYC and AML norms, along with minimizing fraud and securing the online shopping experience.

3. Banks

A bank lies behind a PayFac, conducting checks on the latter’s compliance, submerchant onboarding procedures, and business practices. Before offering customers payment methods from popular card networks (Visa, Mastercard, etc.,) a PayFac must create an account with a sponsor bank.

The bank receives data and money from the card networks and passes them on to the PayFac. In the PayFac model, banks that monitor PayFacs are called Acquiring Banks.

4. Payment processors

Payment processors work in the background, sitting between PayFac’s submerchants and the card networks. Here is a step-by-step workflow of how payment processing works:

- A customer initiates a payment to a sub-merchant using a credit card

- The processor receives the payment authorization request, validates it, and sends it to the card networks

- The card network verifies the transaction and sends an authorization response to the processor

- The transactions are settled by the processor daily and sent to the PayFac’s bank

- After validation, the PayFac’s bank transfers money to the Sub-merchant’s bank

An acquiring bank might host a payment processor, thus combining multiple services under a single roof.

** Related Read: Trends In the Payment Industry for 2022**

If you work in the professional services industry then you likely have heard the buzzword, Fintech over the years.

Fintech, or businesses that combine financial Checking Account Verification Services with technology, have become somewhat of a phenomenon in recent years.

These companies, often from Silicon Valley, are sleek, modern businesses that approach the finance industry with sophisticated technology to optimize business financing processes such as payments, banking, and more.Your business may be approaching this exact situation.

When companies decide that they can handle everything internally or on their own, it can be dangerous and costly.

Not every business Checking Account Owner Authentication will be an expert on each and every factor of running a business.

Outside help is necessary if you want to continue to grow.Click Here