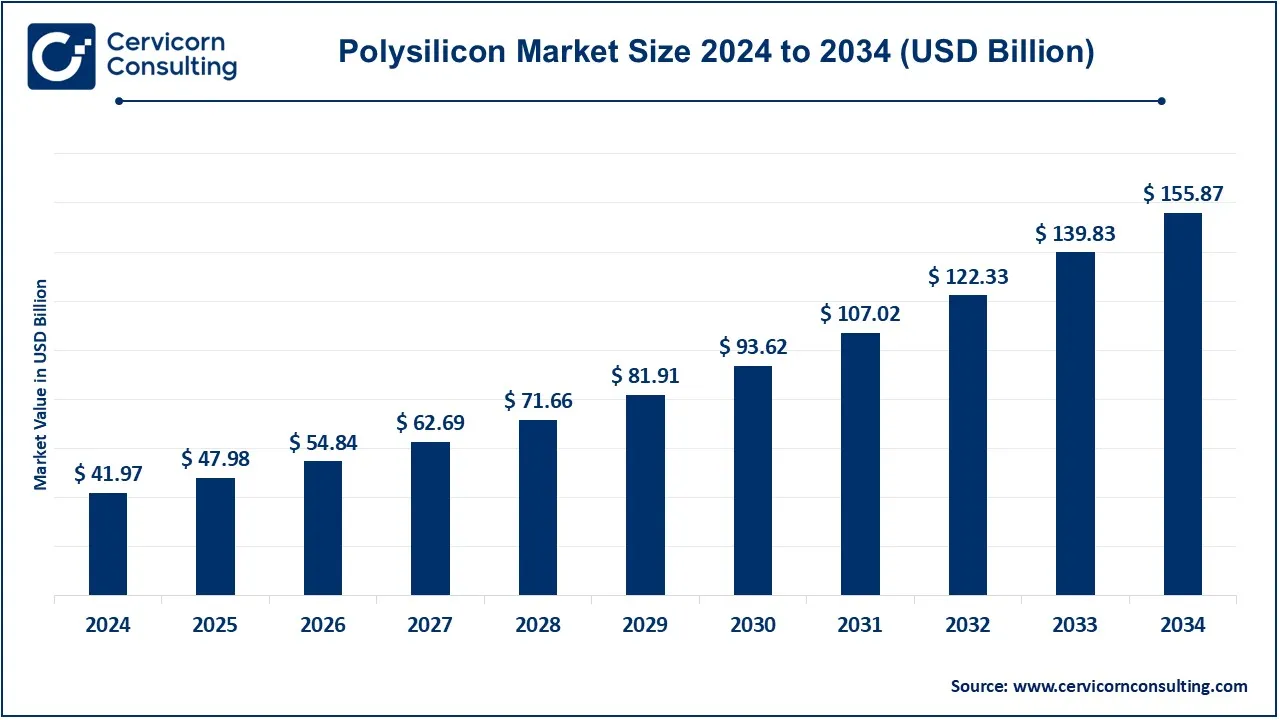

Polysilicon is the unsung hero of the clean energy landscape — a high-purity form of silicon that forms the backbone of solar photovoltaic (PV) cells and semiconductor chips. As the world races toward decarbonization and greater electrification, demand for polysilicon is surging. According to a recent market study, the global polysilicon market was valued at around USD 41.97 billion in 2024 and is projected to reach USD 155.87 billion by 2034, growing at a robust CAGR of 14.30%.

This explosive growth is being driven primarily by the rapid expansion of solar energy capacity worldwide, coupled with rising demand for semiconductors. At the same time, innovation in production technology, geopolitics, and sustainability concerns are reshaping how polysilicon is made and supplied. In this article, we explore the current trends, major drivers, challenges, segmentation, regional dynamics, key companies, and future growth potential in the polysilicon market.

𝐆𝐞𝐭 𝐂𝐮𝐬𝐭𝐨𝐦𝐢𝐳𝐞𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐍𝐨𝐰 👉 https://www.cervicornconsulting.com/sample/2486?utm_source=abhishek

Current Market Trends

1. Explosive Demand from the Solar PV Sector

The solar photovoltaic application dominates the polysilicon market, accounting for over 76% of revenue in 2024. As countries pursue aggressive renewable energy targets, utility-scale and distributed solar installations are driving massive demand for high-purity solar-grade polysilicon.

2. High-Purity Polysilicon for Electronics

While solar remains the largest end-use, the electronics segment (which includes semiconductors) holds a significant share—nearly 24% in 2024. The semiconductor industry increasingly requires ultra-pure polysilicon for wafers used in memory, logic, and power devices.

3. Shift in Polysilicon Forms

Polysilicon is produced in different physical forms: chips, chunks, and rods. As of 2024, chips accounted for 58% of the market revenue, followed by chunks (33%) and rods (9%). This skew reflects increasing demand for materials compatible with modern manufacturing methods, including wafer slicing and ingot growth.

4. Green Production Technologies & Sustainability

Manufacturers are increasingly adopting more environmentally friendly processes, such as fluidized bed reactors (FBR) and optimized Siemens processes, to reduce energy consumption and lower carbon footprints. This trend aligns with global sustainability goals and regulatory pressure.

5. Regional Production & Supply Chain Realignment

Asia-Pacific is the clear leader in polysilicon production, holding 61% of global revenue share in 2024. However, regions like North America and Europe are ramping up capacity to reduce dependency on dominant producers and strengthen local supply chains.

Key Market Drivers

Rapid Growth in Solar Capacity

Deployment of solar PV systems is growing at a breakneck pace. Government policies, favorable financing, and cost reductions are accelerating capacity expansion — all of which fuel demand for polysilicon, the core raw material for solar cells.

Semiconductor Demand Surge

Electronics, electric vehicles (EVs), and data centers are putting pressure on semiconductor supply chains. Polysilicon, particularly ultra-high purity grades, is essential for wafer manufacturing, driving growth in this segment.

Government Incentives & Clean Energy Policies

Many countries are offering subsidies, tax breaks, and favorable regulatory frameworks to support solar power. These incentives boost downstream solar manufacturing, creating long-term demand for polysilicon producers.

Technology Innovations in Production

Advances in manufacturing technologies, such as more efficient chemical processes and energy-saving reactor designs, are reducing production costs. This makes it more feasible to produce polysilicon at scale while maintaining high purity.

Sustainability Push

As ESG (Environmental, Social, Governance) factors become more important, polysilicon manufacturers are under pressure to reduce their carbon emissions and energy usage. Green production methods are emerging as a key differentiator.

Key Market Restraints

Energy-Intensive Production

The traditional methods of producing polysilicon, such as the Siemens process, are highly energy-intensive. Electricity costs make up a significant portion of total production costs, limiting profitability, particularly when energy prices are volatile.

High Capital Expenditure

Building polysilicon manufacturing plants requires heavy capital investment in specialized reactors, purification units, and infrastructure. These high upfront costs can be a barrier to entry for new players.

Overcapacity and Price Volatility

Rapid capacity expansion, especially in major producing regions, risks overcapacity, which could lead to price declines. Such volatility can undermine margins and discourage long-term investments.

Strict Environmental Regulations

While sustainability is a driver, regulatory demands — particularly around carbon emissions and energy consumption — can raise the cost of production and force manufacturers to retrofit or modernize older plants.

Opportunities in the Polysilicon Market

Expansion of Green Polysilicon Production

There is growing opportunity in producing low-carbon or renewable-powered polysilicon. As buyers (including solar module manufacturers) prefer greener inputs, producers who can deliver eco-friendly polysilicon will have a strong competitive advantage.

Vertical Integration into Solar and Semiconductor Sectors

Polysilicon companies can move downstream by integrating with wafer, cell, or module manufacturing. This offers control over the supply chain and higher value capture.

Localized Production and Supply Chain Diversification

By building new capacity outside traditional hubs, like in North America or Europe, producers can tap into governmental incentives, reduce logistics risk, and strengthen supply resilience.

Advanced Polysilicon Grades for Emerging Technologies

Demand for specialty grades of polysilicon—such as ultra-high purity for next-gen semiconductors or specific formulations for high-efficiency solar cells—is rising. Developing and commercializing these grades can unlock premium markets.

Recycling and Circular Economy Models

Recycling silicon materials from end-of-life solar panels and wafers could become a major growth opportunity. Circular models would help reduce raw material demand and align with ESG goals.

Market Segmentation

Understanding the polysilicon market requires breaking it down across key segments:

By Form

Chips: Most widely used; dominant revenue share in 2024

Chunks: Bulk, granular form, often used for various manufacturing steps

Rods: Used in ingot production, particularly for wafer slicing

By Application

Solar Photovoltaics

Monocrystalline solar panels

Multicrystalline solar panels

Electronics

Semiconductors (memory, logic, power, etc.)

By Region

Asia-Pacific

North America

Europe

Latin America, Middle East & Africa (LAMEA)

𝐆𝐞𝐭 𝐂𝐮𝐬𝐭𝐨𝐦𝐢𝐳𝐞𝐝 𝐒𝐚𝐦𝐩𝐥𝐞 𝐍𝐨𝐰 👉 https://www.cervicornconsulting.com/sample/2486?utm_source=abhishek

Regional Market Insights

Asia-Pacific

This region is the undisputed powerhouse in the polysilicon market, accounting for around 61% of global revenues in 2024. China is a dominant force, thanks to vast production capacity and integrated supply chains. Meanwhile, countries like India are scaling up solar installations and local manufacturing, reinforcing the region’s strength.

North America

North America holds about 21% of the polysilicon market. Increasing concerns about supply chain security, coupled with government incentives, are driving investment in domestic polysilicon capacity. Local production helps reduce dependence on imports and mitigates geopolitical risk.

Europe

Europe is emerging as a focused player, especially with its strong commitment to green energy. Renewable mandates, environmental regulations, and recycling initiatives are encouraging investments in sustainable polysilicon. European producers are also aligning with global ESG goals.

LAMEA (Latin America, Middle East & Africa)

Though smaller in share, this region is growing. Investments in solar infrastructure in countries like Brazil and South Africa, along with supportive energy policies in Middle Eastern nations, are opening up new demand for polysilicon. Still, infrastructure and capital raise challenges for faster growth.

Top Companies in the Polysilicon Market

Several major players are leading the polysilicon market in terms of production capacity, innovation, and global reach. Key companies include:

High-Purity Silicon America Corporation

OCI Company Ltd.

Qatar Solar Technologies

REC Silicon ASA

Tongwei Group Co., Ltd.

Tokuyama Corporation

Wacker Chemie AG

Xinte Energy Co., Ltd.

DAQO New Energy Co., Ltd.

GCL-Tech

These firms are investing in both capacity expansion and greener production technologies, and are actively securing offtake agreements across solar and electronics sectors.

Future Growth Potential

Looking ahead, the polysilicon market is poised for transformative growth, driven by several megatrends:

Green Energy Transition

As global solar installations accelerate, especially in emerging markets, polysilicon demand will continue to skyrocket. Combined with rising ESG mandates, green polysilicon production could become standard.

Technological Breakthroughs

Innovations in reactor design (e.g., fluidized bed), novel purification techniques, and energy-efficient processes will lower production costs and environmental impact, making polysilicon more accessible.

Supply Chain Resilience

The geopolitical push for onshoring and decentralizing supply chains will drive capacity building in North America and Europe. This will reduce reliance on concentrated production hubs and improve global supply security.

Semiconductor-Grade Demand

As the demand for chip-grade silicon rises — fueled by 5G, AI, EVs, data centers, and more — polysilicon producers will increasingly focus on ultra-pure grades, leading to higher revenue per unit.

Circular Economy & Recycling

Recycling silicon from retired solar panels, wafers, and manufacturing scrap will become more viable. This will not only reduce raw material dependence but also support sustainability goals.

Strategic Partnerships & Vertical Integration

Polysilicon manufacturers will increasingly partner with wafer, module, or cell producers to lock in demand, reduce risk, and increase value capture.

Conclusion

The global polysilicon market is entering a pivotal growth phase. With a projected rise from nearly USD 42 billion in 2024 to over USD 155 billion by 2034, this sector is being powered by soaring demand for solar PV and high-purity semiconductor applications. While energy-intensive production, capital constraints, and regulatory pressures pose challenges, the opportunities — especially in green production, vertical integration, and advanced materials — are immense.

Leading companies and governments are aligning their strategies around sustainability, supply chain security, and technological innovation. For stakeholders across the clean energy and electronics ecosystems, investing in polysilicon capacity and innovation is not just a commercial play — it’s a strategic imperative for the future of energy.

Buy now at a 10% to 15% discount price: https://www.cervicornconsulting.com/buy-now/2486?utm_source=abhishek

About Us: Cervicorn Consulting specializes in providing expert analysis and accurate market intelligence, helping companies of all sizes make well-informed decisions.

Contact Us:

Phone: +91 7499931916