The global iron and steel market was valued at USD 1,676.24 billion in 2022 and is projected to expand at a compound annual growth rate (CAGR) of 3.8% between 2023 and 2030. The anticipated growth is primarily driven by increasing investments in residential construction. Iron and steel products offer a high strength-to-weight ratio, enabling them to withstand substantial loads and resist compression, tension, and bending forces. These attributes make them particularly suitable for supporting tall structures and efficiently distributing weight to the foundation. Additionally, these materials exhibit excellent durability and resistance to corrosion, weather effects, and pests, contributing to the long-term structural integrity of buildings and reducing ongoing maintenance costs—making them a preferred option in the construction sector.

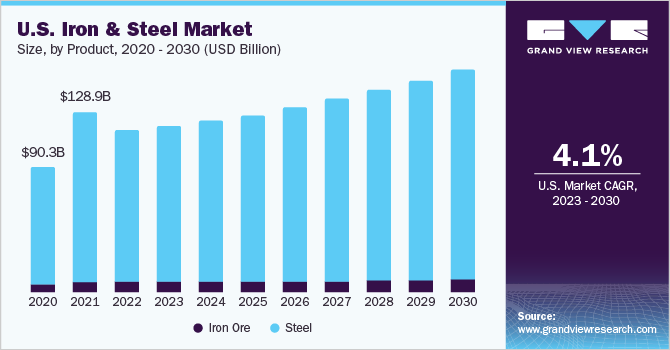

In North America, the United States stands out as a major consumer of iron and steel, owing to heightened demand from key sectors such as construction, infrastructure, automotive, transportation, heavy machinery, and consumer goods. As per the U.S. Census Bureau, total construction expenditure in the country for the first five months of 2023 reached USD 740.8 billion, marking an increase of approximately 2.9% compared to the same period in 2022.

Government initiatives are also anticipated to stimulate demand for domestic iron and steel products. For example, in April 2022, the U.S. government mandated that all iron and steel used in federally funded infrastructure projects under the Job’s Act must be domestically produced. This regulation requires all stages of production, including melting and coating, to be conducted within the United States.

Additionally, increasing demand for heavy machinery is expected to further support product consumption throughout the forecast period. For instance, in May 2023, new orders for manufactured durable goods rose by 1.7%, with transportation equipment orders seeing a 3.9% increase compared to April 2023.

The ongoing Russia-Ukraine conflict has had a negative impact on the iron and steel industry, resulting in significant price hikes. According to the United Nations Conference on Trade and Development, the disruption in the supply of oil, gas, and coking coal from Russia has contributed to a notable rise in global energy prices, which in turn has led to a reduction in the consumption of various iron and steel products across multiple end-use industries.

Get a preview of the latest developments in the Global Iron And Steel Market! Download your FREE sample PDF today and explore key data and trends

Regional Insights

In 2022, the Asia Pacific region accounted for more than 59.0% of the global iron and steel market’s revenue. This dominance is attributed to rising investments in the residential and commercial construction sectors in emerging economies such as China and India. For example, TARC Limited announced a planned investment of INR 250 crore (USD 30.23 million) in 2022 to develop a luxury residential project in New Delhi, India.

North America is expected to post a revenue CAGR of 4.2% during the forecast period. Growing investments in electric vehicle production are projected to boost the demand for iron powder, electric steel, and other related components in the coming years.

Key Companies & Market Share Insights

The market is composed of numerous players, both large and small, operating globally. Many of these companies are pursuing expansion through strategic acquisitions and capacity enhancements. For example, in January 2022, Steel Dynamics acquired a 45% equity interest in New Process Steel. This move is expected to broaden Steel Dynamics’ involvement in value-added manufacturing opportunities. Leading companies in the global iron and steel market include:

Gather more insights about the market drivers, restrains and growth of the Iron And Steel Market

The Iron And Steel Casting Market research report provides the latest industry data, growth, key segments and future trends on the basis of the detailed study.

This market report also allows you to identify the future opportunity and growth rate of the leading segment based on regions and countries.This research report also includes profiles of major companies operating in the global market.

Some of the prominent players operating in the global iron and steel casting market are Amsted Rail Company Inc., ArcelorMittal SA, Calmet, Inc., ESCO Corporation, Evraz plc, Hitachi Metals, Ltd., Hyundai Steel Company, Kobe Steel, Ltd., Nelcast Limited, Nucor Corporation, OSCO Industries, Inc., and Tata Steel Limited.

This section cover profiling of major players in terms of important aspects such as company overview, financial overview, business strategy, and recent developments undertaken during the forecast horizon.Get more information on "Global Iron And Steel Casting Market Research Report" by requesting FREE Sample Copy at https://www.valuemarketresearch.com/contact/iron-and-steel-casting-market/download-sampleMarket DynamicsThe increasing demand for iron and steel casting in automobile and electrical industries owing to their use in the manufacturing of components is driving the market growth.

Furthermore, rising demand for steel casting in the construction industry owing to growing infrastructure-building activities is again fueling the market expansion.

However, the availability of substitute such as aluminum-based alloys casting in several applications may hinder the market growth.The report has been created by using crucial tools such as Porter’s Five Forces Model, Market Attractiveness Analysis and Value Chain analysis to help businesses around the globe navigate opportunities and challenges in the rapidly evolving marketplace with clarity.

Some of the prominent players operating in the global iron and steel slag market are JSW Steel, TMS International Corporation, POSCO, Harsco Corporation, NLMK, TATA Steel, Arcelor Mittal, JFE Steel Corporation, Stein, Inc., Edw.

C. Levy CO., Nippon Steel & Sumitomo Metal Corporation, and Steel Authority of India Limited, finds Transparency Market Research (TMR).

Request Sample pages of premium Research Report: https://www.transparencymarketresearch.com/iron-steel-slag-market.htmlBurgeoning Building and Construction Industry Creating Lucrative AvenuesThe demand for iron and steel slag is driven by a rapidly growing construction industry in various developing and developed regions.

The wide preference of the granulated blast furnace slag material for making Portland blast furnace slag cement is mainly attributed to several benefits such as notable strength over extended duration of use and amazing chemical durability.

Owing to high wear-resistant property, steel making slag is used for aggregate for asphalt concrete.

This is mainly attributed to the pressing demand for sustainable construction materials in the building and construction industry in emerging economies.Specialized Products and Value-added Services Boosting Market Constant advancement in technology has led to production of specialized products, thereby boosting the overall market.