Tail coverage malpractice insurance, often referred to as tail malpractice insurance, is an extended reporting endorsement that allows physicians to report claims even after their malpractice insurance policy has ended. It is specifically designed for claims-made policies, which are the most common type of malpractice coverage in the United States.

In a claims-made policy, coverage only applies if:

The incident occurs while the policy is active, and

The claim is filed while the policy is still active

When a physician leaves a job and the policy ends, any future claims related to past services will not be covered unless legal malpractice tail coverage is in place.

2. Why Tail Coverage Matters When Changing Jobs

Changing jobs is common in the medical field, but it can create a significant coverage gap. Without tail coverage malpractice protection, physicians remain exposed to lawsuits for care they provided in the past.

Medical malpractice claims can take months or even years to surface. For example, a patient may file a claim long after treatment. If your policy is no longer active, you could be personally responsible for legal costs and damages.

This is why understanding tail malpractice insurance is critical before leaving any position.

3. Who Pays for Tail Coverage?

There is no one-size-fits-all answer in the US healthcare system. The responsibility for paying tail coverage depends entirely on the terms outlined in your employment agreement.

In general, payment responsibility can fall on:

The physician

The employer

A shared arrangement

A new employer through alternative coverage

Because of this variability, reviewing your contract carefully is essential before making any job transition.

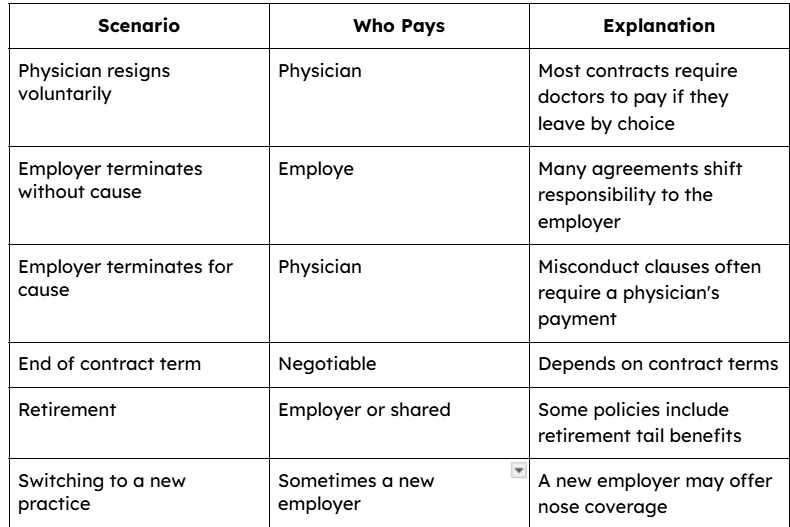

4. Common Scenarios and Payment Responsibility

Below are the most common real-world scenarios that determine who pays for tail coverage malpractice insurance:

5. How Much Does Tail Coverage Cost?

One of the biggest concerns with tail malpractice insurance is the cost.

Typically, tail coverage costs:

150% to 250% of your annual malpractice premium

Example:

If your yearly premium is $12,000:

Tail coverage may cost between $18,000 and $30,000 (one-time payment)

Factors that affect cost:

Medical specialty (high-risk fields cost more)

Claims history

Geographic location within the US

Insurance provider

Because of the high cost, planning ahead is crucial.

6. How to Negotiate Tail Coverage in Your Contract

Negotiating tail coverage upfront can save you thousands of dollars.

Practical strategies:

Ask the employer to cover full tail coverage malpractice costs

Request a vesting schedule (e.g., employer pays more the longer you stay)

Include clauses for:

Termination without cause

Disability or death

Retirement

Example:

“Employer agrees to pay 100% of tail malpractice insurance upon termination without cause or after three years of employment.”

Physicians who negotiate early often avoid significant out-of-pocket expenses later.

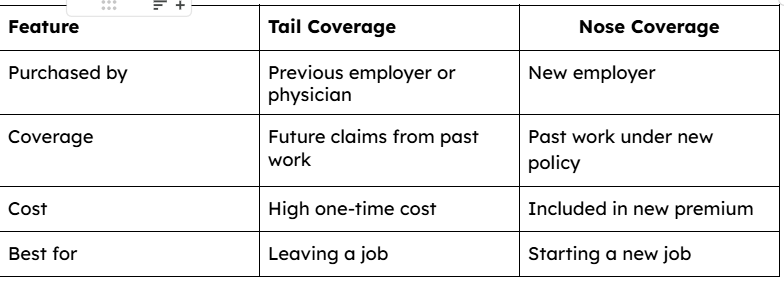

7. Tail Coverage vs. Nose Coverage

When changing jobs, you may also hear about nose coverage (prior acts coverage), which can replace tail coverage.

Nose coverage is often preferred because it eliminates the need to purchase legal malpractice tail coverage separately.

8. Top Medical Malpractice Insurance Companies

Choosing the right insurer is important when evaluating malpractice tail coverage options.

Some of the top medical malpractice insurance companies in the US include:

PLI Consultants

The Doctors Company

MedPro Group

MAG Mutual

Coverys

ProAssurance

These providers offer flexible policy options, including tail coverage, and are known for strong financial stability and claims support.

9. Key Takeaways

Tail coverage malpractice insurance is essential when leaving a claims-made policy

Responsibility for payment depends on your employment contract

Costs can be significant, often 2–2.5 times your annual premium

Negotiating terms upfront can reduce or eliminate your financial burden

Alternatives like nose coverage may provide a more cost-effective solution

Final Thoughts

Understanding who pays for tail malpractice insurance when you change jobs is critical for protecting your financial future. Many physicians overlook this detail until it’s too late, leading to unexpected costs and coverage gaps.

Before making any career move, carefully review your contract, explore negotiation options, and compare coverage alternatives. Being proactive ensures you remain protected from future claims while maintaining peace of mind throughout your medical career.

Working with experienced advisors like PLI Consultants can also help simplify the process. They specialize in guiding physicians through malpractice insurance decisions, including tail coverage malpractice insurance, ensuring you choose the right protection based on your career stage and risk profile.