To be eligible for a deduction for child care expenses, the child must be charged to you.

- If you have the child looked after away from your home (nursery or daycare center or approved nursery assistant):

a tax credit equal to 50% of the expenses paid for the care (excluding food costs and deduction of family help received under of custody) is applied to the expenses child tax credit income limit you incur for the care of your children aged under 6 at 1 st January of the income year (children born after 31 December 2013 for the imposition of income for the year 2020 declared in 2021).

The expenses taken into account include salaries and social contributions paid to the childminder.

If you live in a common-law union, only the parent who has the dependent child can benefit from the tax credit provided that the supporting documents for the sums paid are established in his name. However, in the event that the burden of supporting the child is shared and neither of the two parents can justify having the main charge, the amount of the tax credit is divided by two.

Expenses are limited to $2,300 per child in care ($1,150 if the child is in alternate residence or shared care).

You must indicate these expenses under the heading “Childcare costs for children under six years old” If you declare online, the amounts paid in 2020 for these expenses and which you declare via the PAJEMPLOI system will be reminded to you in order to help you to declare the corresponding amounts. - If you have the child looked after at your home:

You can claim the tax credit for amounts paid for home employment. For more details, you can refer to the information you will find in the section "Personal services".

As part of the withholding tax, the tax credit (childcare costs for young children or employment of an employee at home) is part of the mechanism known as the "reduction advance and tax credit". Thus, the tax credit that will be granted to you in the summer of 2021 for expenses paid in 2020 will give rise to the payment of a deposit of 60% of the amount of this tax credit in January 2022. During the liquidation of income tax for 2021 in 2022, the advance paid will be reduced by the tax credit that you may have on the basis of expenses incurred in 2021 (in 2021 you will therefore have received 100% of the credit of tax to which you are entitled: 60% in January, and the remainder in the summer).

Schooling of children

When your dependent or attached child pursues secondary child tax credit income limit or higher studies in a public or private establishment on December 31 of the tax year (December 31, 2020 for the 2020 income tax), you can benefit from an income tax reduction.

Note: education must lead to the issuance of a diploma (general, technological, vocational or university training, excluding continuing education qualification courses). In addition, teaching must be provided collectively and full-time in an establishment (with, where appropriate, work-based training). Finally, students must not be bound by an employment contract, nor be paid and must be free from any commitment during and at the end of their studies.

The amount of the tax reduction is set at:

- $ 61 per child pursuing lower secondary studies (college);

- $153 per child pursuing upper secondary studies (lycée);

- $183 per child following higher education training.

In the case of children in alternating residence or with shared responsibility, the amount of the tax reduction is halved.

Compensatory allowance

You can benefit from a tax reduction if you are domiciled in France and if you pay in execution of a divorce judgment, a divorce agreement approved by the judge or a divorce agreement by mutual consent without homologation by the judge, a compensatory capital allowance all at once or in installments within a period not exceeding 12 months from the date on which the judgment becomes final.

The tax reduction is equal to 25% of the amount of payments made, goods or rights allocated, withheld within the limit of $30,500 for the entire 12-month period.

When you pay a compensatory allowance partly in the form of an annuity and partly in the form of cash capital released within 12 months of the divorce, you do not benefit from the tax reduction. On the other hand, you retain the possibility of deducting from your taxable income the amount of pensions paid, in respect of alimony.

When the tax reduction is applicable, the sums received by the beneficiary of the service are not subject to income tax.

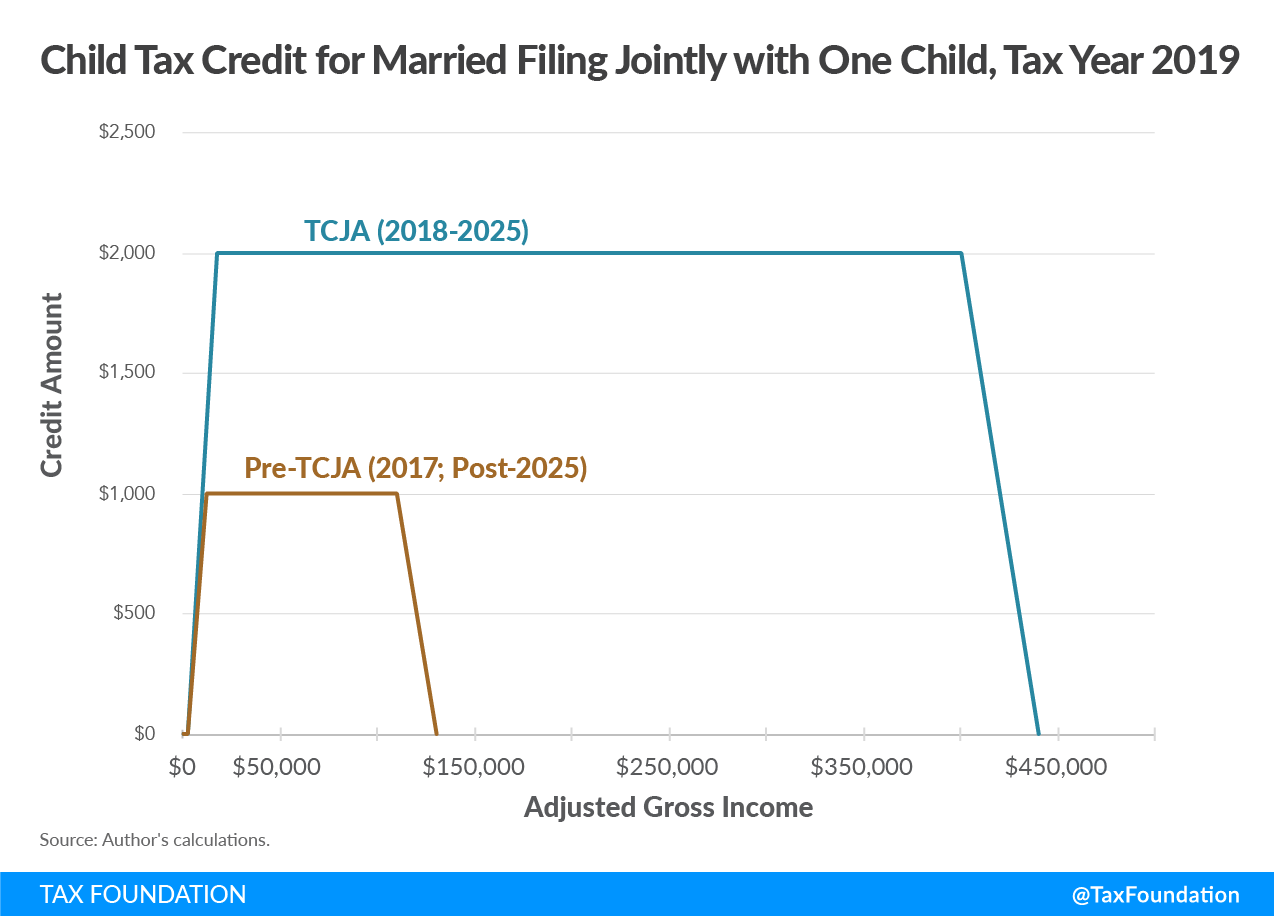

As we have mentioned above, the child tax credit was started by the U.S. President in March 2021.

Under this tax benefit, the highest child tax benefit is $3,600 only for children below 6 years of age.

Also, the adjusted gross income should be less than $1,50,000 or $75,000 for both individuals.

Further, the added tax benefit will be discontinued for those who pay taxes but earn more money.

On the other hand, the benefit will cease for those who earn $95,000 and the married couple who earn $1,70,000 and file taxes jointly.

The official sources will take 2020 tax returns into use to ensure eligibility.

At times when money is needed urgently, and you cannot wait weeks for your loan or credit card application to be processed, an easy option is Instant Approval Cards.

Just give us a missed call on 022 6181 6111 to explore our unique Free Advisory Service.

The holder can pay back the entire borrowed amount at the end of each month, or a minimum fixed amount.

This is required to show a proof of steady income to be able to pay the credit card bill.

Credit History: Credit history is a record of how the applicant manages credit related activities.

The APR gives a general idea on how much you pay for availing the card and facilitates in comparing different issuers.