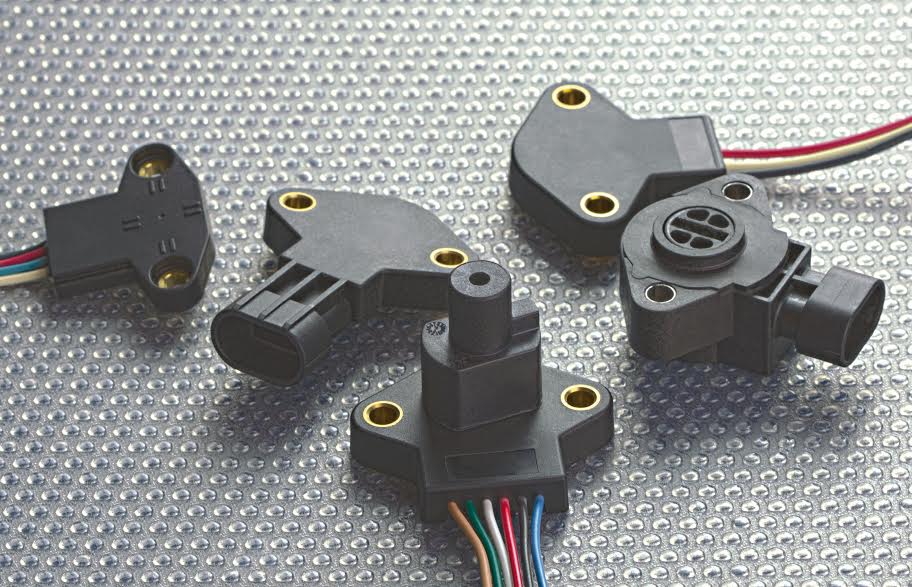

Position sensors are critical devices used to detect the movement, location, and orientation of objects across a wide range of industries. These sensors—encompassing technologies such as potentiometric, magnetic, optical, and capacitive types—provide precise measurements that drive automation, improve safety, and enhance operational efficiency in manufacturing, automotive, aerospace, and robotics applications. Advantages include high resolution, repeatability, low maintenance, and seamless integration with control systems, enabling real-time feedback for motion control and predictive maintenance.

Position Sensor Market Industry 4.0 and the Industrial Internet of Things (IIoT) continue to shape manufacturing processes, demand for compact, high-performance position sensors has grown significantly. Where manual monitoring once slowed production, intelligent sensor solutions now facilitate streamlined workflows, boost quality assurance, and support data-driven decision making. Adoption of these sensors helps organizations address market challenges related to downtime and process variability, while capturing new market opportunities in smart factories and electric vehicles.

The position sensor market is estimated to be valued at USD 6.36 Bn in 2025 and is expected to reach USD 10.41 Bn by 2032, growing at a compound annual growth rate (CAGR) of 7.3% from 2025 to 2032.

Key Takeaways

Key players operating in the Position Sensor Market are Vishay Intertechnology, Inc., Siemens AG, Sick AG, Sensata Technologies, and Schneider Electric SA.These market companies account for significant industry share, leveraging extensive R&D investments and strategic partnerships to strengthen their market position and expand product portfolios.The market presents ample market opportunities driven by the rise of electric and autonomous vehicles, demand for precision robotics, and expansion of renewable energy projects. With growing emphasis on predictive maintenance and remote monitoring, manufacturers can capitalize on these trends to develop next-generation sensor solutions that target energy efficiency and reduced lifecycle costs.

Market insights also reveal untapped potential in aftermarket retrofits and customization services for legacy equipment, further widening the scope for business growth and sustainable revenue streams.Global expansion is evident as emerging economies in Asia Pacific and Latin America ramp up industrialization. North America remains a mature market with steady growth, underpinned by advanced manufacturing and aerospace sectors. Europe, propelled by stringent safety regulations and smart factory investments, continues to drive market growth. Meanwhile, Middle East and Africa are gradually adopting digitalization, presenting new avenues for sensor deployment in oil & gas, infrastructure, and mining applications. These dynamics underscore the broad market forecast and market segments defined by region, application, and technology.

Market DriversRapid industrial automation stands out as a key market driver for position sensors. As manufacturers strive for higher throughput, lower operating costs, and consistent product quality, they increasingly rely on automated machinery equipped with precise sensing components. Position sensors provide indispensable feedback loops in servo systems, robotic arms, and conveyor lines, ensuring accurate motion control and reducing human intervention.

The integration of sensors with PLCs and distributed control systems enhances overall system reliability and supports predictive maintenance strategies that minimize unplanned downtime. Furthermore, the convergence of advanced analytics and IIoT platforms amplifies the value of sensor-generated data, allowing real-time monitoring of equipment health and performance. This synergy between hardware and digital solutions fuels market growth, with organizations seeking robust, low-power, and miniaturized sensors that adapt to evolving production demands. By addressing both operational efficiency and safety requirements, industrial automation continues to propel global demand for position sensors across diverse end-use sectors.

PEST Analysis

Political: Government policies promoting industrial automation and stringent safety regulations are driving adoption of position sensors across sectors such as manufacturing and energy. Trade agreements and tariff frameworks affect supply chain resilience, prompting firms to diversify sourcing strategies. Incentives for digital infrastructure upgrades encourage private investment in smart factories, while periodic regulatory reviews necessitate ongoing market research to ensure compliance. Political stability in key manufacturing nations reduces the risk of disruptions and supports steady capital allocation.

Economic: Fluctuations in raw material prices and currency exchange rates influence production costs for sensor components, impacting profit margins and competitive pricing. Strong growth in automotive output and renewable energy installations fuels demand, while global economic slowdowns can temporarily dampen capital expenditures on automation projects. Access to low‐cost financing and government stimulus packages in emerging markets bolsters industrial expansion. Shifts in labor costs and tax policies further shape procurement decisions and manufacturing footprints.

Social: Growing focus on workplace safety and environmental sustainability is encouraging end users to integrate precise monitoring solutions, supporting broader corporate responsibility goals. Increasing consumer awareness of product reliability fosters trust in advanced sensing technologies. Demographic trends, such as urbanization and aging populations, are driving demand for automated healthcare equipment and smart mobility solutions. Educational initiatives highlighting STEM skills are expanding the talent pool available for sensor R&D and calibration services.

Technological: Rapid advancements in IoT connectivity and device miniaturization are shaping product design philosophies in the position sensor industry. These innovations spur collaborative R&D and generate fresh market opportunities in sectors such as automotive, robotics and healthcare.

Geographical Concentration of Value

North America, Western Europe and parts of East Asia collectively account for the most significant value concentration in the position sensor arena, benefiting from established industrial ecosystems and strong capital investment flows. In North America, the United States leads with a dense cluster of automotive OEMs, aerospace contractors and automation integrators that rely heavily on precise position detection to optimize production and ensure safety. Canada contributes through its resource extraction and heavy machinery sectors, where ruggedized sensors are critical for equipment monitoring. Market insights underscore how local R&D centers, supported by favorable intellectual property regimes, catalyze the development of next-generation sensing solutions, reinforcing regional market share.

Western Europe, anchored by Germany and France, remains a powerhouse due to its robust manufacturing base and early adoption of Industry 4.0 strategies. The presence of leading industrial automation companies and extensive testing facilities accelerates product validation cycles. These factors, combined with well-developed transportation infrastructure, strengthen supply-chain efficiency and distribution networks. Market trends reveal that European consumers’ stringent quality expectations drive sensor manufacturers to maintain high standards in calibration and reliability, sustaining premium pricing and greater revenue per unit.East Asia’s concentration of value is propelled by major electronics hubs in Japan and South Korea, where high-precision manufacturing demands top-tier sensing performance.

Advanced robotics deployment in semiconductor fabrication plants and automotive factories fuels consistent volume purchases. Strategic government programs supporting smart factory rollouts further enhance market opportunities. Although cost pressures persist, local development of novel materials and manufacturing processes is improving competitiveness. This combination of strong industrial demand, innovation ecosystems and government backing cements East Asia’s role as a core value center in the global position sensor landscape.

Fastest Growing Region

The Asia Pacific region is currently experiencing the most rapid expansion in the position sensor domain, driven by dynamic industrial growth and digital transformation initiatives across several emerging economies. China, India and Southeast Asian nations are aggressively investing in smart manufacturing, renewable energy, and advanced mobility, all of which depend on precise position detection technologies. In China, national programs focused on “Made in China 2025” and similar modernization plans are catalyzing widespread adoption of automated assembly lines and intelligent robotics, creating substantial market opportunities.

Local OEMs and system integrators are partnering with global sensor companies to develop tailored solutions, reflecting a blend of international expertise and regional cost advantages.India’s shift toward Industry 4.0, supported by government incentives and private sector ventures, is creating a fertile environment for new sensor deployments in automotive, rail transport and process industries. Rapid urbanization and infrastructure development projects, such as smart cities and metro rail networks, rely on position sensors for tunnel boring machines, crane operations and platform screen doors.

Market dynamics in this subregion highlight a trend toward integrated sensing platforms that combine position, temperature and vibration data, offering enhanced functionality and reducing system complexity.Southeast Asia, encompassing Malaysia, Thailand, Vietnam and Indonesia, is emerging as a significant hot spot for expansion due to rising domestic manufacturing activity and increasing foreign direct investment in electronics and automotive component facilities. The presence of special economic zones and technology parks fosters collaboration between international sensor companies and local startups, accelerating innovation cycles.

Local demand for automation in electronics assembly, food and beverage processing, and pharmaceuticals is rising, driven by the need for higher throughput and quality control.Across the Asia Pacific, improving infrastructure, supportive regulatory reforms and expanding talent pools are lowering barriers to market entry. This has intensified competition among regional and global players, leading to aggressive product localization and strategic alliances. Market trends indicate the introduction of wireless and predictive maintenance-capable sensors will further boost adoption rates, reinforcing the region’s position as the fastest growing segment in the global position sensor market.

Get this Report in Japanese Language: 位置センサー市場

Get this Report in Korean Language: 위치센서시장

About Author:

Ravina Pandya, Content Writer, has a strong foothold in the market research industry. She specializes in writing well-researched articles from different industries, including food and beverages, information and technology, healthcare, chemical and materials, etc. (https://www.linkedin.com/in/ravina-pandya-1a3984191)

Impact of COVID-19 on Industrial Automation MarketCOVID-19 pandemic has caused a severe impact on the global economy at various levels and the impact is seen on the Industrial automation market as well.

Inferable from the emergency brought about by the pandemic, the production, and supply chain activities have experienced a minor slump.

They have utilized various industry-wide unmistakable business merge estimations, figures, and market information into income assessments and projections in the Automatic Die Cutting Machines Market.

Key Players Global Automatic die cutting machines Market Participants Some of the market participants identified across the value chain of global automatic die cutting machines market are:Focus Technology Co., Ltd.Zhejiang Feida Machinery Co.,LtdAssociated Pacific.DiecutGlobalNatraj Corrugating Machinery CoVailankanni InternationalKirti Engineering WorksSuba Solutions Private LimitedVisit For TOC >> https://www.futuremarketinsights.com/toc/rep-gb-7834Segmentation Global automatic die cutting machines market can be segmented on by type, by processing material, end use industry and by region.On the basis of type, the global Automatic die cutting machines market can be segmented as:Fully AutomaticSemi-AutomaticOn the basis of processing material, the global Automatic die cutting machines market can be segmented as:PaperPlasticTextileLatherMetalOther Materialsautomobile industry, medical & pharmaceutical industry, textile industry, manufacturing, and other industrialOn the basis of end use industry, the global Automatic die cutting machines market can be segmented as:Automobile IndustryMedicalPharmaceutical IndustryGraphics and DesignTextileProduct Segmentation The investigation offers a top to bottom evaluation of different clients' journeys pertinent to the market and its segments.

The study endeavors to assess the current and future development possibilities, undiscovered roads, factors that shape their income potential in the global market by breaking it into di such as its types, applications, and region-wise assessment.

By Type Applications Regions CoveredInsights in the Report Full in-depth analysis of the parent market FMI analysts follow industry-wide, quantitative customer insights and methodologies for demand projection to produce results.

Receiving and dispatching inventory can be a complex process.

There is a need to minimise dock-to-stock time effectively through docking equipment that easily removes shipments from freight trucks.Armstrong, one of India's biggest industrial automation companies have the exact cost-efficient solution for these pain points.Speed, accuracy and reliability are the keys for the distribution systems.

The businesses like Retail, E-tail and Express Courier undergo constant disruptions.

Flexible solutions that make their processes and operations easy are hence a vital necessity.An integrated warehouse automation solution to tackle these problems and stay ahead of the curve are Graffias & Tegmine.http://armstrongltd.com/dock-automation.php